Myth-Busting: Lowell is a scam artist

Is Lowell a scam artist or trickster? Answer: Absolutely not. Lowell is a legitimate company, that’s authorised by the Financial Conduct Authority.

Read moreAt Lowell, we know that there are lots of money myths floating about and it can be hard to know whether to believe them or not. So, as part of our mission to help improve financial education, we want to uncover the truth behind common money myths that you may have heard before.

Research conducted here at Lowell has revealed that 20% of Brits say that they can’t make well-informed financial decisions due to a lack of money knowledge, which only highlights the importance of being careful.

So, let’s find out which common money myths Brits are most likely to believe and whether they’re true or not.

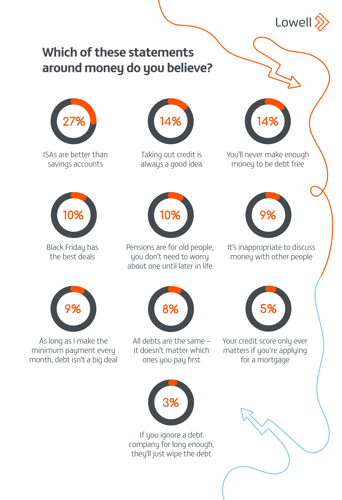

Over a quarter (27%) of Brits said that they believe ISAs are better than savings accounts – the most common money myth believed across our research.

Both have different purposes with different benefits, there are different types of ISAs and savings accounts to choose from. Whether you’re trying to put some money aside for a larger purchase or save for a rainy day, it’s important to put your money in the right account for you.

Individual Savings Accounts (ISAs) are tax-free, meaning you’re able to save money without paying any income tax. The two main types of ISAs are cash ISAs and stocks and shares ISAs. However, there is a maximum amount of money you can put into an ISA each tax year, which is currently £20,000 for anyone aged over 16.

With standard savings accounts, any interest earned may be taxed depending on your circumstances. There’s also no limit to how much money you can put into a savings account each tax year, unlike an ISA. However, it’s worth noting that some savings accounts may have restrictions when it comes to withdrawals so you should always check before putting your money in.

When you’re in need of some extra money, you might think about borrowing. In fact, 14% of Brits we surveyed are under the impression that taking out credit is always a good idea.

While taking out credit and paying it on time and in full can have a positive impact on your credit score, if you’re already in debt or struggling with your finances, taking out further credit could make things worse and result in problem debt. To find out more about the impact that taking out credit can have, you can read our guide on how your credit file affects you.

We know that being in debt can feel overwhelming, and our survey found that nearly 1 in 6 (14%) Brits feel they’ll never make enough money to be debt-free.

At Lowell, our customers come first, and we believe that becoming debt-free shouldn’t be difficult, which is why our repayment plans are affordable and based on your individual circumstances. If you’re a Lowell customer and have any concerns about your debt, our team are always there to listen and will work with you to find a solution. We want to make things as simple as possible and you can easily manage your account with us online or via our app.

Once you’ve set up a payment plan with your creditor, you’ll have a minimum amount that you have to pay back each month. According to our research, 1 in 10 (10%) people believe that debt isn’t a big deal as long as you make the minimum payment every month.

Many lenders will only require you to just pay the minimum on your debt repayment plan each month, however paying only the minimum will also mean it takes longer to clear your debt and you will pay more interest in the longer term. This is also not always the best approach as you might be charged higher interest rates depending on who you have the debt with.

At Lowell, our payment plans are based on the individual circumstances of our customers. If you’ve got a debt with Lowell, please get in touch with us and we’ll look at your plan together.

If you’re like 10% of the Brits we surveyed, you’ll likely be under the impression that your pension is only something you need to start thinking about in later life.

Pensions are there to help you save money for after you retire and are no longer earning a regular income. So, while you might not access the money until you’re older, the point is to start saving earlier and build up a healthy pension pot. To find out more, MoneyHelper has a useful guide on why you should save into a pension.

We understand that if you’re in debt or struggling with your finances, it might be hard to talk about your circumstances with someone else, with 9% of respondents saying that they think it’s inappropriate to discuss money with other people.

At Lowell, we want to remove the stigma that surrounds this, with our guide on how to talk to a loved one about debt including helpful tips and conversation starters.

If you’ve got a debt with Lowell, you can always speak with our friendly team who are trained to be considerate of your situation. Alternatively, if you don’t feel comfortable getting in touch with us, there are other organisations where you can seek independent advice and support.

Regardless of whether you’ve got one debt or more, you might think that the goal is to become debt-free, and 8% of those we spoke to think that all debts are the same and it doesn’t matter which ones you pay off first.

If you’ve got multiple outstanding debts in your name, there are certain debts which should be cleared first. These are also known as priority debts and are important to pay off first because they could cause you serious problems if not paid. Priority debts can include:

Once you’ve cleared all your priority debts then you can start focusing on your other ‘non priority debts’ for example credit or store card debt. If you’re unsure where to start or which debts you should clear first, Citizens Advice can offer free and unbiased guidance.

1 in 20 respondents (5%) said that they believe their credit score only matters when applying for a mortgage. While your credit score plays a large role when applying for a mortgage, is this the only time it matters?

Your credit file can affect you in other ways, including your ability to borrow any additional money in the future, and may even impact how favourable the interest rates you receive. That’s why it’s important to understand your credit file as well as how to improve your credit score.

We understand that you may feel worried or overwhelmed when first contacted by a debt company like Lowell, especially if you weren’t already making payments towards your debts. In fact, 3% of Brits presume that if you ignore a debt company for long enough then they’ll just wipe your debt.

Ignoring debt companies does not mean they’ll wipe your debt, something which we’ve explored further in our guide on what happens if you ignore a debt company.

When a debt company doesn’t hear back from you, they’ll continue to try and reach out through letters, calls, emails and texts and may even work with third parties to do so. If you’ve heard from us at Lowell, please do get in touch so we can work together to find a solution whatever your circumstances.

Here at Lowell, we’re always here to help and support our customers however we can. If you’ve got a question relating to your Lowell debt, then you can get in touch with our team who will be happy to listen and support you.

Our debt guidance hub also includes a wide range of helpful guides covering a range of debt-related topics and the way Lowell works with customers. We’ve also created our debt dictionary to help you understand technical financial terms and confusing jargon.

Published by Stephanie North-Shaw on 15 May 2023

Is Lowell a scam artist or trickster? Answer: Absolutely not. Lowell is a legitimate company, that’s authorised by the Financial Conduct Authority.

Read moreHave you ever worried that a company might use the info you share against you? We won't do that, so let us explain how your details are safe with us.

Read moreFind out who we are, what we do and why we feel becoming debt-free should be simple and affordable.